Mobile credit card processing allows businesses to accept in-person payments away from a countertop checkout terminal. Mobile payments help manage long queues, keep your operations efficient, and offer customers convenient ways to pay — all without sacrificing data security or system stability.

Based on our evaluation, the best mobile credit card processing solutions for 2024 are:

Company

Our Score (out of 5)

Monthly Account Fee

Fee Structure

Mobile Processing Options

Helcim

4.53

$0

Interchange plus rates

Mobile Card Reader + App Smart Terminal

Square

4.44

$0–$89 (w/ POS)

Flat rate w/ option for custom pricing

Mobile Card Reader + App Smart Terminal

PayPal Zettle

4.36

$0–$30

Flat rate w/ option for custom pricing

Mobile Card Reader + App Smart Terminal

Clover

4.35

$0–$49.95 (w/ POS in paid plan)

Depends on processor

Mobile Card Reader + App Smart Terminal

Stax

4.33

$99–$199

Wholesale interchange rate

Mobile Card Reader + App Smart Terminal

CardX

4.30

$29–$199

Flat rate for debit card payments

Web-based platform Smart Terminal

Helcim: Best overall mobile credit card processing solution

Overall Score

4.53/5

Pricing

5/5

Mobile app features

5/5

Support & Reliability

4.38/5

User Experience

4/5

Average User Review Scores

4.13/5

Pros

- Mobile-optimized payment and POS software

- Automated volume discounts

- Free credit card processing program

- HIPAA-compliant for healthcare services

Cons

- Add-on fees for Amex transactions

- Third-party POS integration requires custom APIs

- Does not support tap-to-pay on iPhones

Why I chose Helcim

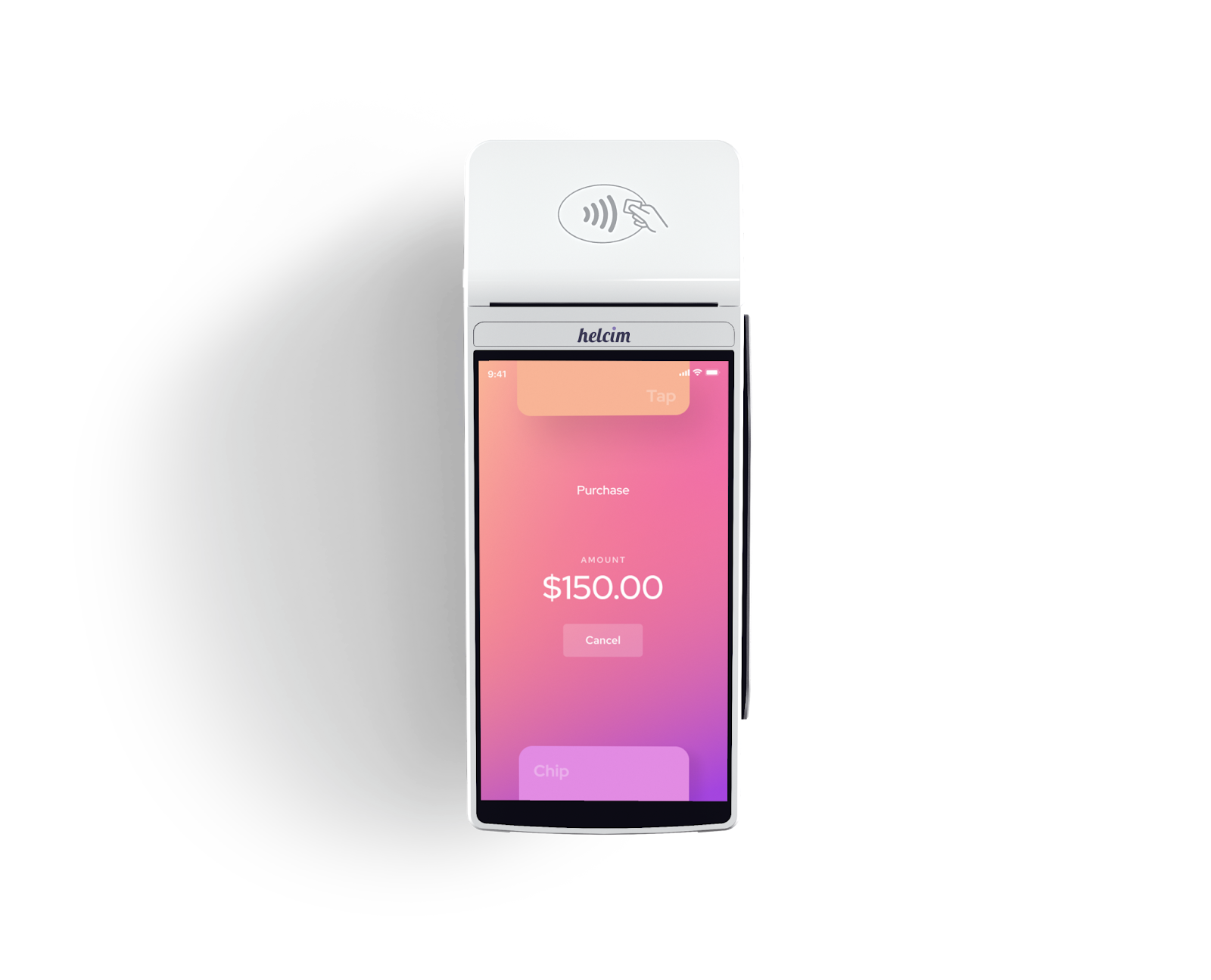

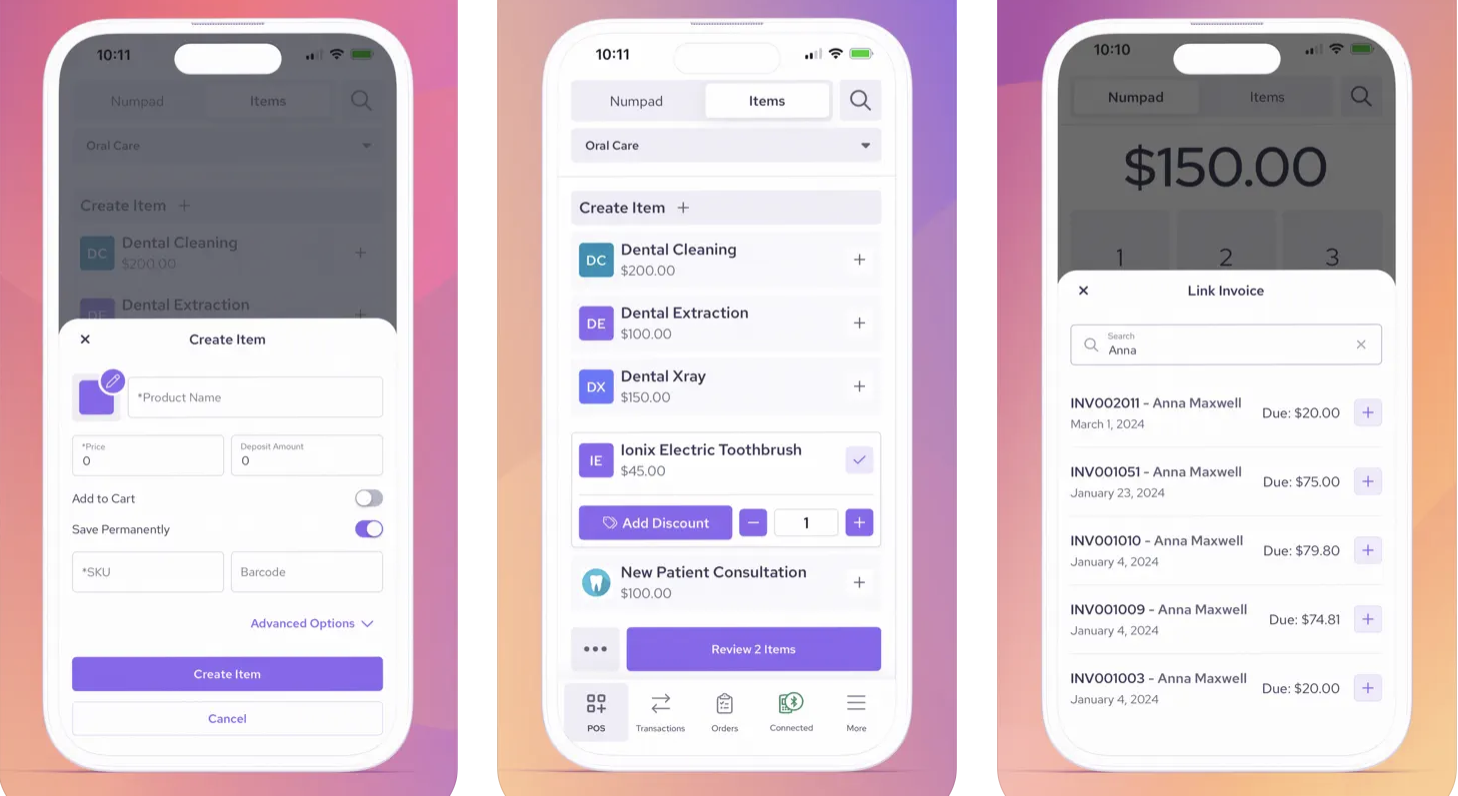

Helcim is a traditional merchant services provider that also offers simple POS software. It provides an app-based mobile payment platform, as well as a mobile payment terminal with a built-in POS. The smart terminal also has a built-in free credit card processing program (via surcharging) for in-person transactions. While the terminal is on the expensive side, Helcim does offer installment payment plans.

Helcim has several great features for growing businesses. For one, it offers an interchange plus fee structure with built-in volume discounts, so there is no need to apply for better rates at every milestone. The system is also HIPAA-compliant, so it can securely process healthcare service transactions. Helcim’s simple upgrades for its POS are limited, but custom APIs allow companies to integrate Helcim with other business software.

Helcim’s mobile credit card processing features are ideal for growing businesses. Its automated functionalities help maximize savings while providing scalability via developer-based customization.

- Mobile card reader and app: The Helcim mobile credit card reader pairs with a mobile POS app that’s compatible with both iOS and Android. The card reader comes with a PIN Pad for added security when processing card transactions.

- Smart terminal: Helcim’s standalone smart terminal can process swiped, dipped, and tapped credit card payments. It has built-in POS software, a thermal receipt printer, and a surcharging option that’s easy to toggle on and off for each transaction.

- Payment services: Helcim’s POS and payment software are HIPAA-compliant. The smart terminal supports invoicing and manual entry payments, while the mobile POS app can set up recurring billing and accept payments via a built-in virtual terminal.

- Fee-saving options: Helcim provides automated volume discounts based on 3-month rolling sales. The payment software also supports level 2 and 3 data processing with an interchange optimization feature. The smart terminal also has built-in free credit card processing functionality via surcharging, which passes the processing fees onto customers.

- Customizations: Helcim’s POS offers limited pre-built integrations, but its payment processing software can be integrated into a business’ custom software via developer tools and APIs.

- Monthly account fee: $0

- Card-present fee: Interchange plus 0.15% + $0.06 to 0.4% + $0.08

- Card-not-present fee: Interchange plus 0.15% + $0.15 to 0.50% + $0.25

- American Express transactions: Additional 0.10% + $0.10

- Virtual terminal fee: $0

- Chargeback fee: $15 (refundable)

- Hardware cost: $99–$329 or $29 for 12 months

- Application/set up fee: $0

- Cancellation fee: $0

Square: Best for retail, wholesale, and restaurants

Overall Score

4.44/5

Pricing

3.44/5

Mobile app features

4.75/5

Support & Reliability

4.69/5

User Experience

4/5

Average User Review Scores

4.67/5

Pros

- Built-in industry-specific POS solution

- HIPAA-compliant software

- CBD program for cannabis sellers

- Available customizations for enterprise-level businesses

Cons

- Not compatible with other software

- Primarily flat rate fees, custom rates by request

- Limited customer support hours

Why I chose Square

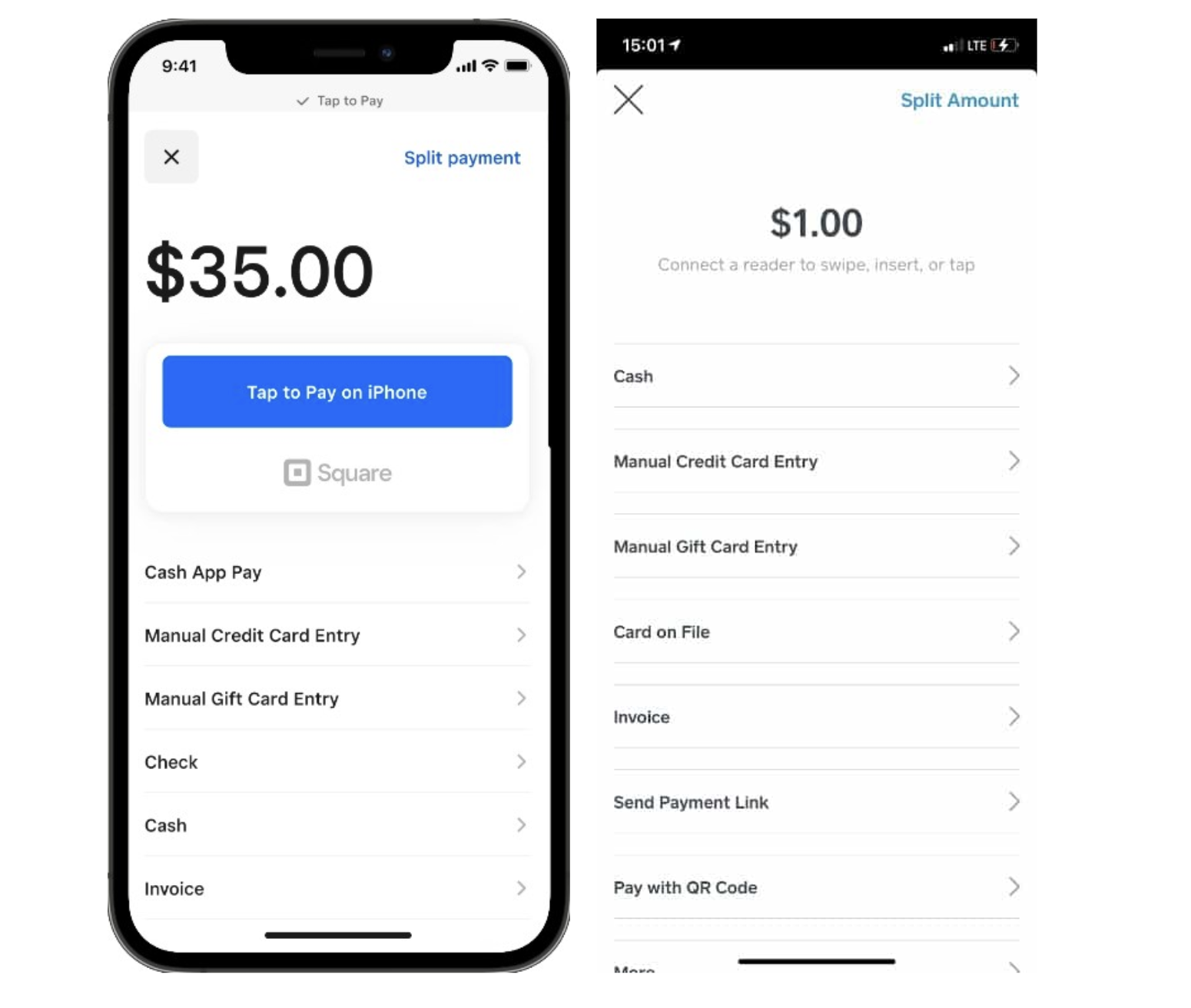

Square is a popular all-in-one POS system with a built-in payment processing feature. New and small businesses love Square because it allows them to set up and start selling with little to no upfront cost. Square offers a mobile credit card processing solution with a free mobile POS app, mobile credit card reader, and stand-alone POS terminal. It even waives up to $250 worth of chargeback fees every month.

That said, Square has also grown into efficient business software for large retailers. It offers custom rates for businesses with sales of more than $250,000 a year and uses developer APIs to connect with existing software. The Square Terminal with the built-in POS offers mobility and is perfect for large-volume sales in warehouses. Square is even HIPAA compliant (like Helcim) and can process payments for CBD businesses.

In addition to dedicated retail services, Square also offers solutions tailored to the restaurant industry. Its mobile card readers and terminals can support food trucks, cafes, and restaurants of all sizes.

Square’s mobile credit card processing features consist of app-based mobile software and a POS terminal with built-in payment tools. Custom integrations are available for growing businesses.

- Mobile credit card reader and app: Square’s mobile credit card readers connect with the free Square mobile POS app. The magstripe reader (first is free) is separate from the contactless and accepts all types of in-person payment methods, including tap-to-pay on iPhone.

- Smart terminal: The Square Terminal comes with built-in POS software and a thermal printer. It also includes a customer display that allows for custom tipping, customer feedback, and email signup for digital receipts and loyalty program enrollment.

- Payment services: In addition to point-of-sale transactions, Square’s software is equipped with invoicing, recurring billing, ecommerce, and virtual terminal tools. It can process EBT/Snap payments as well as healthcare transactions with its HIPAA compliance.

- Fee-saving options: Square offers volume discounts for businesses that process more than $250,000 in annual sales. Enterprise-level businesses can negotiate for custom rates and payment services.

- Customizations: Square offers a complete ecosystem of additional business tools and third-party integrations for small businesses. For larger companies, Square provides custom integrations via developer APIs to connect with their current business systems.

Read more: Different Types of POS Systems

- Monthly account fee: $0–$89 (includes POS software)

- In-person fee: 2.6% + $0.10

- Online fee: 2.9% + $0.30

- Keyed-in fee: 3.5% + $0.15

- Custom pricing: Sales volume greater than $250,000 annually

- Virtual terminal fee: $0

- Chargeback fee: Waived up to $250/month

- Hardware cost: $0–$299

- Application/set up fee: $0

- Cancellation fee: $0

PayPal Zettle: Best for global and peer-to-peer payments

Overall Score

4.36/5

Pricing

3.13/5

Mobile app features

4.75/5

Support & Reliability

4.38/5

User Experience

4.25/5

Average User Review Scores

4.57/5

Pros

- Known and trusted brand

- Global payment methods

- Instant deposits to your PayPal account

- Mobile credit card terminal for custom business software

Cons

- Lacks offline payment processing

- Dispute management feature is an add-on

- Reputation for poor customer support

Why I chose PayPal

PayPal is a well-known and trusted mobile-first payment processing platform for individuals and small businesses. Its peer-to-peer payment capabilities and instant access to funds via its digital wallet make PayPal one of the easiest to use, particularly for occasional sellers. In recent years, PayPal has made great strides in expanding its payment services to provide features for growing and large businesses.

PayPal Zettle replaced PayPal Here, PayPal’s former point-of-sale app, to provide improved in-person payment processing tools such as a stand-alone POS terminal equipped with a barcode scanner. With PayPal’s global payment methods, this particular mobile hardware will work great for selling at large trade shows and exhibits. For large businesses, PayPal also adds a modern mobile card reader that can easily be integrated with advanced customization tools designed to create a flexible payment ecosystem.

PayPal’s mobile credit card processing features consist of two mobile credit card readers with a built-in PIN pad, one that works with a mobile POS app and the other with custom software for larger businesses. There is also a smart POS terminal with optional accessories for scalability.

- Mobile credit card reader and app: PayPal Zettle provides a simple mobile credit card reader that connects to a mobile POS app. A modern mobile card terminal is also available for large businesses.

- Smart terminal: PayPal Zettle’s smart terminal comes with the PayPal POS software. Optional upgrades available for a barcode scanner, thermal printer, and countertop dock.

- Payment services: In addition to the standard swipe, chip, and contactless payments, PayPal Zettle can accept Tap to Pay, PayPal, Venmo, Apple Pay, Google Pay, and Samsung Pay. The mobile POS software is also equipped with invoicing, recurring billing, and virtual terminal tools.

- Fee-saving options: Volume discounts with interchange plus pricing are available for larger businesses using custom payment features via Braintree.

- Customizations: Large businesses can also use PayPal’s Braintree customization tools to create a flexible payment ecosystem via unified payment solutions, payment optimization, and payment orchestration.

Read more: Learn how PayPal stacks up against Square.

- Monthly account fee: $0

- In-person: 2.29% + $0.09

- Online fee: 2.59% + $0.49

- Keyed-in fee: 3.49% + $0.09

- Custom rates: Volume-based custom flat rate and interchange plus pricing

- Virtual terminal fee: $30 per month

- Chargeback fee: $15–$20

- Mobile hardware cost: $29–$299

- Application/set up fee: $0

- Cancellation fee: $0

Clover: Best for payment processor flexibility

Overall Score

4.35/5

Pricing

4.38/5

Mobile app features

4.25/5

Support & Reliability

4.69/5

User Experience

4.25/5

Average User Review Scores

3.8/5

Pros

- POS software with built-in payment features

- Compatible with multiple payment processors

- Customizable checkout flow

- Can process payments offline

Cons

- Contract terms vary

- Hardware cannot be reprogrammed

- Scalability depends on the processor

Why I chose Clover

Clover is a POS software provider that also offers proprietary hardware with built-in payment processing tools. The system is owned by Fiserv (formerly First Data) and, by default, applies Fiserv rates when purchased directly through Clover. That said, Clover’s unique value proposition is that the software and hardware are resold through ISOs and resellers on the Fiserv network, including popular processors such as Stax, PaymentCloud, and Dharma Merchant Services.

This means that businesses can choose from a number of payment processors to use Clover, each offering different contract terms, risk tolerances, additional services, and fee structures. Clover is also equipped with developer-based and API customization tools, plus a list of third-party custom integration services to scale the system and meet large business needs. However, it is important to note that once purchased and programmed, Clover hardware cannot be reprogrammed to work with a different processor, so choose wisely.

Clover offers proprietary hardware that includes a mobile credit card reader and a smart POS terminal. The system can even process payments without an internet connection. Both the mobile POS app and the built-in POS can be customized to upgrade their features for large businesses.

- Mobile credit card reader and app: Clover’s mobile credit card reader can process chip and contactless payments. It works with a mobile POS app that supports tipping, full or partial refunds, returns, and exchanges.

- Smart terminal: Clover Flex comes with built-in POS software and can process swipe, chip, and contactless transactions. The hardware can be programmed with, or pre-built if purchased from, your preferred payment processor.

- Payment services: Clover’s mobile terminal is equipped with invoicing and virtual terminal features. It can also be integrated to accept online orders and process online sales.

- Fee-saving options: Transaction fees will depend on the business’ preferred payment processor, which may offer additional tools such as surcharging and level 2 and 3 data processing. This means rates can be flexible and still use Clover’s software and hardware system.

- Customizations: Clover offers developer tools and third-party integration service partners that businesses can use to customize payment features.

- Monthly account fee: $0–$59.95 (paid plan includes POS software)

- Card-present fee: Depends on the processor

- Card-not-present fee: Depends on the processor

- Chargeback fee: Depends on the processor

- Mobile hardware cost: $49–$599 or $35 for 36 months

- Application/set up fee: Depends on the processor

- Cancellation fee: Depends on the processor

Stax: Best for large-volume sales and scalability

Overall Score

4.33/5

Pricing

4.69/5

Mobile app features

4.5/5

Support & Reliability

4.06/5

User Experience

4.5/5

Average User Review Scores

3.93/5

Pros

- Wholesale subscription rates

- Payment services for SaaS platforms

- All-in-one API for customizations

- Billing and surcharging tools for large businesses

Cons

- Limited mobile hardware options

- Terminal protection fee on top of equipment cost

- Lacks same-day funding functionality

Why I chose Stax

Stax is a traditional merchant service offering wholesale subscription rates, which are ideal for midsize to large businesses. It is our top choice for scalability because everything about Stax is designed to keep up with growing demands for payment features and services. Businesses can choose from a range of options, from hardware to customization tools.

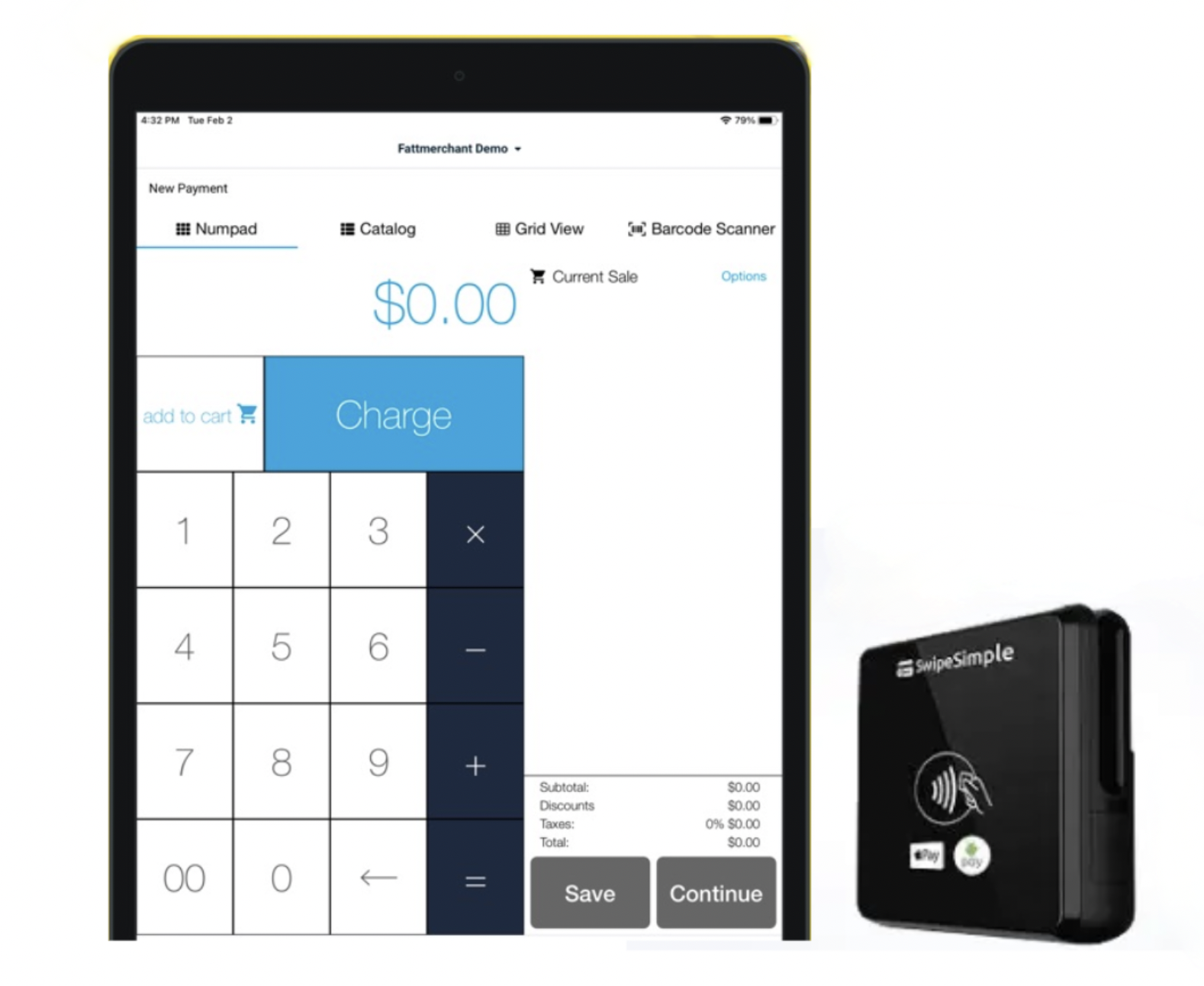

This means even its mobile payment processing service can be customized to match unique business needs. Stax has the SwipeSimple mobile card reader configured to work with the Stax Pay mobile app. It also supports Dejavoo and Clover smart terminals for businesses that need more advanced payment features while accepting payments on the go, such as tableside ordering and sales in restaurants. Stax’s payment technology is also equipped with tools to integrate with proprietary business software.

Stax mobile credit card processing features start with Stax Pay software available on a mobile app and built into its smart terminals. Businesses have a choice between Dejavoo and Clover Flex hardware, which can be customized to include advanced payment features.

- Mobile credit card reader and app: Stax pairs its Stax Pay mobile app with the SwipeSimple mobile credit card reader that accepts swipe, dip, and tap credit card payments.

- Smart terminal: Dejavoo and Clover Flex are available for Stax users. Both hardware brands can print paper receipts and have the ability to accept swipe, EMV, and contactless payments. It provides a customer display function that can capture signatures, set custom tips, and allow customers to input their email addresses for digital receipts.

- Payment services: Stax supports invoicing, recurring billing, and virtual terminal features. It can also be programmed to include surcharging tools and multi-currency payments.

- Fee-saving options: As it is, Stax already provides wholesale interchange rates via subscription-based pricing. Surcharging can also be programmed and level 2/3 upon request for businesses that qualify for B2B rates.

- Customizations: Stax provides various products for optimizing payment services for larger businesses. Stax Connect offers developer tools to customize payment features on SaaS platforms. Stax Processing offers simplified payment technology to customize payment services and connect with proprietary software for large businesses.

- Monthly account fee: $99–$199

- Card-present fee: Interchange + $0.08

- Card-not-present fee: Interchange + $0.18

- Virtual terminal fee: $0

- Hardware cost: Contact Stax for pricing

- Chargeback fee: $25

- Application/set up fee: $0

- Cancellation fee: $0

CardX: Best for surcharging

Overall Score

4.3/5

Pricing

4.06/5

Mobile app features

4.75/5

Support & Reliability

4.06/5

User Experience

4.5/5

Average User Review Scores

3.5/5

Pros

- Exclusive Mastercard surcharging partner

- Auto surcharging for in-person transactions

- Works in conjunction with other payment processors

- Volume-based monthly plans

Cons

- Limited mobile hardware options

- Customizations depend on payment processor

- Lacks same-day funding

Why I chose CardX

More and more payment processors are offering surcharging capability, and the service is becoming increasingly popular with merchants and other businesses. However, CardX remains the most reliable. CardX is an active participant in shaping surcharging laws in the U.S., making it THE expert in surcharging compliance. It offers surcharging programs for both online and in-person transactions while working with other payment processors.

CardX uses the Dejavoo smart terminal to accept in-person credit and debit card payments. The hardware comes with CardX’s payment platform, which supports invoicing and subscription management. CardX does not have app-based software, but its web platform is mobile-optimized, so users can make manual entry payments from a mobile device. CardX can operate alongside other payment processors, including those that cater to larger businesses like Stax.

Although CardX’s mobile credit card processing features are limited to a standalone smart terminal, the system works with other payment processors that can provide additional payment tools.

- Fully compliant surcharging program: CardX offers fully compliant surcharging features to businesses in 48 states plus the District of Columbia. Additional terms apply to companies operating in the states of Maine and New York.

- Smart terminal: CardX provides pre-programmed Dejavoo smart terminals to businesses that want to apply surcharging. Like other Dejavoo hardware, it is equipped with a thermal printer and customer display function that allows for custom tipping, signature capture, and PIN debits.

- Payment services: The CardX payment platform includes built-in invoicing, recurring billing, and virtual terminal functions. Users can also initiate transactions from the CRM.

- Fee-saving options: CardX allows businesses to significantly lower credit card processing fees with the surcharging feature, which passes processing fees on to customers. Transaction fees for when customers use their debit cards can go lower depending on the payment processor.

- Customizations: Except for Lightbox, which can be used to customize online checkout forms, CardX does not offer any other customization options. That said, CardX can work with other payment processors that support customization features.

Read more: While Stripe did not make our list, Helcim, Square, PayPal, and CardX are all top Stripe alternatives.

- Monthly account fee: $29–$199

- Card-present fee: From 2.91% for debit card payments or based on payment processor

- Card-not-present fee: From 2.91% for debit card payments or based on payment processor

- Virtual terminal fee: $0

- Hardware cost: $375–$540 (plans available)

- Chargeback fee: $0

- Application/set up fee: $0

- Cancellation fee: $0

Key components of mobile credit card processors

Mobile credit card processing solutions consist of several components that work together to provide the flexibility businesses need to maximize sales.

The most important factor to begin with is the mobile hardware. Without it, businesses would be unable to expand their sales processing away from a fixed checkout terminal. Providers should ideally have different options, from standard mobile credit card readers to full-on stand-alone payment terminals. The hardware should be durable and reliable to avoid any delays in processing transactions.

Businesses will also need mobile payment software that goes along with the hardware. App-based mobile software (on a smartphone or tablet) that connects with a mobile credit card reader is the most popular option. On the other hand, smart terminals are becoming increasingly popular, as they come with their own built-in platform programmed by the payment processor.

These mobile software include POS solutions with varying degrees of functionality. While some allow for just basic payment processing, others come equipped with full inventory management and CRM solutions.

Connectivity is also an important component when using mobile payment software. Businesses need a smartphone or tablet that supports Bluetooth to connect the mobile payment app with the mobile credit card reader. Internet connection via WiFi or data is also required to actually process payments.

Benefits of mobile credit card processing

Mobile credit card processors allow businesses to process sales tableside, curbside, and in other locations outside a brick-and-mortar shop, such as pop-up stores, food trucks, farmers markets, trade shows, and exhibits. This helps bust lines, reduce wait times, and provide a great customer experience.

Additionally, mobile credit card processors are designed for ease of use. The user interface is very similar to how smart devices work (even easier with payment apps installed on a smartphone or tablet), which means employees require minimal training to start processing sales.

Mobile credit card processing is also a cost-effective alternative to traditional setups. Mobile payment apps are often free, and some are even equipped with robust POS software at no extra cost. Most card readers are inexpensive and at times, offered for free or at a discount. If you’re looking to purchase an all-in-one smart terminal instead of pairing a smartphone with a mobile reader, many solutions, such as Square, offer interest-free installment plans on hardware purchases.

Lastly, mobile credit card processors are highly scalable. In addition to easily adding more terminals, mobile payment software can be integrated with a larger business system and even upgraded with advanced payment processing features.

Also read: Best Tablet POS Systems and Best Mobile POS Systems

Challenges of mobile credit card processing and how to overcome them

Challenge: Connectivity issues that disrupt transactions on mobile credit card processors.

Solution: Make sure there is a reliable internet connection and anticipate poor WiFi, especially when selling on the go. Be prepared with a data plan on your mobile device and consider providers that offer offline payment functionality.

Challenge: Hardware malfunction caused by limited battery life, card reader disconnection, accidental drop, or water damage during operations.

Solution: Research reviews from real-life users before purchasing hardware. Invest in high-quality mobile credit card readers/terminals and accessories such as protectors, backup batteries, and portable chargers.

Challenge: Security concerns resulting in chargebacks and compromised sensitive customer information.

Solution: Work only with Level 1 PCI-compliant payment processors. Monitor staff activity using mobile credit card terminals that support multi-user logins. The mobile card reader should be compatible with EMV chip cards and, ideally, PIN pads to ensure that customer data is encrypted during transactions.

Finding the best mobile credit card processor for you

When choosing a mobile credit card processor, the most important factor to consider is the system’s ability to provide a reliable and efficient mobile payment solution. The best mobile payment processor should, therefore, be flexible with its payment methods, cost-effective, durable, and have the ability to scale its features as your business grows.

Helcim is among the most versatile mobile credit card processors on the market. Its best asset is the ability to automate nearly all of its payment functions (including applying discounts) and customize its features with developer tools for larger businesses.

Square and PayPal are solid runners-up. Square is known for its extensive POS features, and PayPal offers a range of payment methods. Both are favorite mobile processors for new and small businesses, but they both also offer advanced customization capabilities to cater to enterprise-level sales.

Clover and Stax are on our list because of their versatility. Companies in various industries can rely on Clover’s compatibility with payment processors like Stax that offer advanced features and better transaction rates.

CardX seamlessly integrates with other payment processors that provide scalable payment services while allowing businesses to significantly minimize their costs.